The financial services landscape is experiencing its most profound structural shift since the dawn of digital banking. Artificial intelligence is no longer an experimental line item in innovation budgets; it has become the fundamental architecture of competitive advantage. Modern global financial ecosystems handle data volumes that are entirely beyond human capacity to process in real time.

Traditional financial operations rely on historical, batch-processed data, which creates systematic friction, slows down decision-making, and leaves institutions vulnerable to fast-evolving fraud networks. By introducing intelligent automation and predictive analytics, AI shifts the financial sector from a reactive posture to a predictive, real-time operating model. Leading organizations are leveraging these technologies to radically compress operational timelines, reduce overhead, and design highly personalized user experiences that protect margins and capture market share. For institutional depth and strategic frameworks across emerging technology domains, you can explore the insights and research published on AIUniverse.

Featured Snippet

What Is AI in Finance?

AI in finance is the strategic integration of machine learning, predictive analytics, natural language processing, and generative models within financial operations. It automates complex processes, accurately identifies anomalous behavior for fraud mitigation, optimizes high-frequency trading strategies, assesses credit risks, and delivers hyper-personalized customer experiences across banking, insurance, and investment sectors.

Understanding AI in Finance

Definition of AI in Finance

At its core, AI in finance refers to the deployment of advanced computational models designed to mimic human cognitive functions—such as learning, reasoning, analyzing, and problem-solving—applied directly to financial datasets. Instead of relying on static, hard-coded software rules, AI systems continually parse unstructured and structured data to refine their own execution parameters.

Evolution of Financial Technology

The financial technology lifecycle has evolved through three distinct waves:

[ FinTech 1.0: Analog to Digital ] ──► [ FinTech 2.0: Mobile & Cloud ] ──► [ FinTech 3.0: Intelligent AI Ecosystems ]

(Ledgers, Mainframes) (Apps, APIs, Digital Banking) (Predictive, Agentic, Real-Time)

Traditional financial technology changed how data was stored and moved. Modern AI changes how that data is interpreted and acted upon.

Why Financial Institutions Are Adopting AI

Institutions are adopting AI to solve the problem of data fragmentation and escalating operational costs. Market research from 2026 shows that over 90% of global finance functions have deployed or are actively evaluating AI-enabled technologies. This widespread adoption is driven by the immediate need to process millions of transactions per second, meet strict regulatory mandates, and counter sophisticated cyber threats that bypass legacy security systems.

The Relationship Between AI, Data, and Financial Decision-Making

Financial decisions depend entirely on speed-to-signal—the velocity at which an institution can extract actionable insights from raw data. AI models act as a processing engine that converts massive, unstructured data pipelines (alternative market data, legal contracts, customer behaviors) into clean risk-reward vectors, minimizing human bias and compressing research cycles from days to milliseconds.

In Simple Terms

Think of AI in finance as a super-analyst that never sleeps. It can read millions of pages of financial documents, scan every credit card transaction on Earth instantly, and spot hidden patterns in data that human eyes would miss.

Real-World Example

When you apply for a credit card online and receive an approval or denial within 45 seconds, an AI engine has parsed your credit history, cross-referenced alternative data points, assessed your default probability, and made a risk decision instantly.

Common Mistake

The Data Fallacy: Assuming that buying an advanced AI model will automatically solve operational inefficiencies. An AI model is only as good as the underlying data pipeline. If your data is fragmented across legacy database silos, the model will output inaccurate predictions.

Key Takeaways

- AI shifts financial institutions from a reactive, batch-processed model to a predictive, real-time posture.

- Modern financial data volume requires automated cognitive systems; human oversight alone is no longer scalable.

- Competitive advantage is defined by platform coherence—how smoothly data flows into operational AI models.

Core Technologies Powering AI in Finance

Machine Learning (ML)

- Definition: Algorithms that improve their performance automatically by analyzing statistical patterns in historical data without explicit programming.

- Purpose: To identify hidden correlations within massive datasets and generate predictive outputs.

- Finance Applications: Credit underwriting scoring, dynamic asset pricing, and churn prediction models.

- Business Impact: Drastically reduces manual underwriting overhead and uncovers subtle risk indicators that traditional credit scoring misses.

Deep Learning

- Definition: A subset of machine learning based on multi-layered artificial neural networks designed to mimic human brain processing structures.

- Purpose: To extract high-level, abstract features from highly complex, non-linear datasets.

- Finance Applications: High-frequency algorithmic trading execution and advanced biometric authentication.

- Business Impact: Enables autonomous, microsecond-level market execution, capturing alpha in volatile trading environments.

Natural Language Processing (NLP)

- Definition: Technology that enables computers to interpret, analyze, and understand human language.

- Purpose: To extract structured metrics from vast quantities of unstructured text.

- Finance Applications: Automated regulatory filing analysis, financial news sentiment mining, and legal contract review.

- Business Impact: Compresses investment research timelines by extracting critical insights from thousand-page documents in seconds.

Predictive Analytics

- Definition: The use of historical data, statistical modeling, and ML techniques to forecast future outcomes.

- Purpose: To determine the mathematical probability of future market or customer trends.

- Finance Applications: Loan default forecasting, cash flow management optimization, and customer lifetime value modeling.

- Business Impact: Reduces non-performing loans (NPLs) and optimizes liquidity allocations across institutional accounts.

Generative AI (GenAI)

- Definition: Deep learning models trained on vast datasets capable of generating novel text, code, synthetic data, or financial scenarios.

- Purpose: To synthesize complex financial narratives and generate highly contextual content.

- Finance Applications: Synthetic financial data generation for stress testing, automated investment memo drafting, and conversational portfolio summaries.

- Business Impact: Saves senior finance professionals up to 6–10 hours per week on routine drafting and research tasks, shifting human capital to high-judgment roles.

Computer Vision

- Definition: Software that processes, analyzes, and extracts meaning from visual data like images and videos.

- Purpose: To automate physical and visual verification processes within financial operations.

- Finance Applications: Remote Know Your Customer (KYC) identity verification and satellite imagery analysis for insurance property assessments.

- Business Impact: Lowers identity fraud rates during digital onboarding while reducing physical insurance claims inspection costs.

In Simple Terms

Machine learning finds patterns, deep learning handles complex data, NLP reads human text, predictive analytics guesses what happens next, and generative AI writes summaries or code. Together, they form the brain of modern fintech.

Real-World Example

Investment firms use NLP to scan hundreds of corporate earnings call transcripts simultaneously. The AI detects subtle changes in an executive’s phrasing or tone, converting that linguistic data into a market sentiment score that influences trading strategies.

Common Mistake

Over-reliance on Generative AI for Mathematics: Treating GenAI models as calculation engines. GenAI is built for language generation and context synthesis. For precise quantitative calculations, it must be paired with structured symbolic math tools or traditional programmatic calculator engines.

Key Takeaways

- Different AI tools solve different problems; NLP handles text, while machine learning handles numbers.

- Generative AI’s core benefit in finance is accelerating research workflows and document synthesis.

- Combining multiple AI core technologies yields the highest operational return on investment.

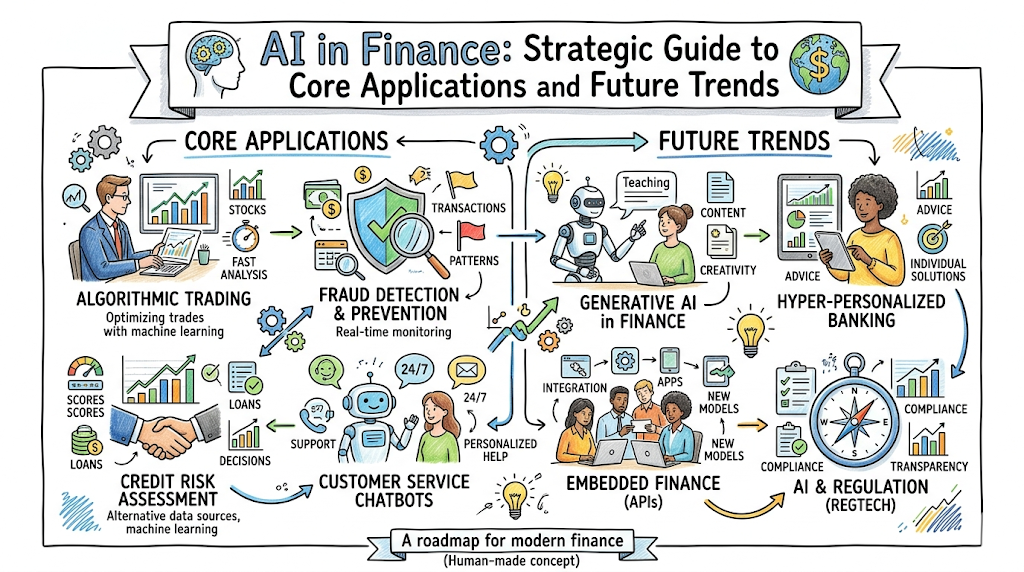

Major Applications of AI in Finance

Fraud Detection and Prevention

- Business Problem: Transaction fraud costs financial institutions billions annually. Legacy rule-based systems generate high false-positive rates, frustrating legitimate clients.

- AI Solution: ML models analyze millions of transaction variables in real time, assessing location, velocity, and behavioral history to catch anomalies.

- Benefits Achieved: Fraud losses drop by up to 50%, while false positives decline significantly, improving client trust.

- Real-World Example: Global payment processors deploy streaming AI pipelines that evaluate fraud risks for credit card transactions within 200 milliseconds, stopping fraudulent charges at the point of sale.

Credit Scoring and Risk Assessment

- Business Problem: Traditional credit scoring frameworks lock out thin-file borrowers who lack deep institutional banking histories.

- AI Solution: Machine learning models evaluate alternative data streams, including utility billing histories, cash flow patterns, and educational background metrics.

- Benefits Achieved: Expands credit approval rates safely by 15–20% without increasing the portfolio’s underlying default rate.

- Real-World Example: Neobanks leverage alternative data models to offer lines of credit to unbanked individuals, validating risk profiles via consistent monthly cash flow behaviors.

Algorithmic Trading

- Business Problem: Financial markets move too quickly for human traders to execute trades at optimized prices across fragmented global order books.

- AI Solution: Deep learning algorithms process real-time market data Feeds, order book depths, and macro news signals to place trades autonomously.

- Benefits Achieved: Maximizes execution speed, minimizes slippage costs, and identifies micro-arbitrage opportunities across global exchanges.

- Real-World Example: Quantitative hedge funds use reinforcement learning models that adjust trading parameters autonomously as liquidity conditions shift throughout the day.

Portfolio Management

- Business Problem: Manually adjusting multi-asset portfolios to match changing market conditions and individual risk tolerances is slow and prone to errors.

- AI Solution: Predictive analytics platforms continuously balance portfolios based on correlation changes, macro factors, and investor goals.

- Benefits Achieved: Provides institutional-grade, risk-adjusted returns tailored precisely to unique risk profiles.

- Real-World Example: Asset management platforms use AI-driven engines to rebalance institutional portfolios daily, hedging against downside risks before market drops occur.

Customer Service and AI Chatbots

- Business Problem: Retail banking call centers face massive call volumes, resulting in long hold times, high staffing costs, and uneven customer satisfaction.

- AI Solution: Generative AI-powered conversational assistants handle multi-step customer inquiries with deep context retention.

- Benefits Achieved: Automates over 70% of routine customer service inquiries, lowering support center overhead.

- Real-World Example: Major consumer banks deploy conversational assistants that safely help users lock cards, dispute charges, and analyze monthly spending patterns via natural language dialogue.

Loan Processing and Underwriting

- Business Problem: Commercial and retail mortgage underwriting requires manual document verification, extending approval cycles to weeks.

- AI Solution: AI-driven document intelligence systems extract, verify, and cross-match income and tax data across complex financial forms.

- Benefits Achieved: Compresses loan closing times from 30 days down to under 48 hours, lowering origination costs.

- Real-World Example: Mortgage lenders deploy intelligent automation pipelines to parse corporate tax returns, validating debt-to-income metrics instantly against underwriting criteria.

Regulatory Compliance (RegTech)

- Business Problem: Evolving global financial regulations overwhelm manual legal and compliance departments, increasing compliance risk.

- AI Solution: NLP engines scan international regulatory updates continuously, mapping changes to internal operating policies.

- Benefits Achieved: Mitigates risk of regulatory oversight and dramatically reduces compliance mapping labor costs.

- Real-World Example: International investment banks use AI platforms to track updates across hundreds of jurisdictions, flagging policy compliance gaps in real time.

Anti-Money Laundering (AML)

- Business Problem: Money laundering schemes span multiple banks and countries, hiding within millions of legitimate wire transfers.

- AI Solution: Graph neural networks (GNNs) analyze relationships across accounts, uncovering complex structuring and hidden networks.

- Benefits Achieved: Doubles the detection rate of hidden criminal financial networks while reducing compliance alert noise.

- Real-World Example: Global banking networks use relationship-mapping AI to track funds moving through shell companies, exposing laundering patterns before final withdrawal.

Financial Forecasting

- Business Problem: Traditional corporate financial planning and analysis (FP&A) relies on narrow, historical data tables, producing inaccurate forecasts during volatile market shifts.

- AI Solution: Time-series machine learning models integrate macroeconomic indexes, supply chain indicators, and consumer demand signals.

- Benefits Achieved: Improves corporate revenue and cash flow forecasting accuracy by 25–30%.

- Real-World Example: Multinational enterprises use predictive forecasting platforms to optimize treasury cash allocations across global subsidiaries, maximizing yield.

Personalized Banking Services

- Business Problem: Standardized banking interfaces treat all customers identical, missing cross-selling opportunities and lowering digital platform engagement.

- AI Solution: Real-time recommendation engines analyze unique spending habits, cash cushions, and life events to serve context-aware insights.

- Benefits Achieved: Increases digital conversion rates for native financial products while strengthening customer loyalty.

- Real-World Example: Mobile banking applications push predictive notifications advising users to move idle cash into yield-bearing accounts based on upcoming bills.

In Simple Terms

AI works like a digital engine installed across banking pipelines. It watches for thieves, updates investment portfolios, reads regulatory updates, reviews loan applications, and answers support tickets all at the same time.

Real-World Example

When a customer travels abroad and buys a coffee, an AI fraud engine instantly evaluates if the purchase aligns with their historical patterns, device location data, and current flight bookings to approve the charge without a lock.

Common Mistake

Treating AI as a Standalone Auditor: Relying on automated AML and fraud alerts without human investigators. AI surfaces complex anomalies, but human compliance experts are required to handle filings and make nuanced ethical decisions.

Key Takeaways

- AI reduces fraud losses by identifying complex anomalies across millions of transactions in real time.

- Alternative data scoring allows underbanked populations to access secure lines of credit.

- RegTech applications significantly lower compliance costs for cross-border financial entities.

AI in Banking

Intelligent Customer Support

Modern retail banks deploy AI assistants that understand context and user intent. These are not old-school, click-based chat tools; they use advanced language models to guide users through complex tasks like setting up travel alerts or tracking down specific past transactions using everyday language.

Automated Loan Approval

By integrating digital data verification APIs with automated risk engines, banks remove human bias from the initial underwriting process. The system instantly evaluates applicant data against risk parameters, accelerating approvals for low-risk clients.

Transaction Monitoring

AI systems run constantly in the background, analyzing transactions as they occur. By learning the normal spending footprint of individual clients, these engines flag strange behaviors—such as simultaneous logins from different countries—to block account takeovers.

Personalized Banking Experiences

Instead of generic interfaces, AI-driven banking platforms display custom dashboards based on user habits. A frequent investor sees prominent market tracking tools, while a small-business owner sees automated cash flow projections and invoice management features.

Operational Efficiency

Behind the scenes, banks use AI to automate repetitive back-office work, like matching signatures on documents, transferring data between legacy software programs, and checking account balances during audits.

AI in Investment Management

Robo-Advisors

Robo-advisors make wealth management accessible by using algorithms to build and manage diversified asset portfolios. Users complete an initial digital risk assessment, and the automated platform allocates and balances capital across low-cost ETFs without charging expensive advisory fees.

Portfolio Optimization

Institutional asset managers use AI engines to run thousands of portfolio simulations based on complex risk metrics. These engines adjust allocations across asset classes to maximize returns for a target volatility level, adapting as market correlations change.

Market Prediction

By processing alternative datasets—such as global cargo shipping logs, retail foot traffic patterns derived from mobile data, and raw commodity production metrics—machine learning models help investment teams spot macroeconomic inflections ahead of standard public reports.

Sentiment Analysis

AI text tools analyze public sentiment across millions of data points, including social media platforms, regulatory disclosures, and financial news sites. These sentiment indexes serve as early leading indicators of momentum shifts in specific stocks or asset classes.

Automated Trading Systems

These platforms execute complex, multi-legged trading strategies at the best possible prices. They break large institutional block orders into tiny, timed transactions across different dark pools and public exchanges, minimizing market impact and preventing front-running.

AI in Insurance

Claims Processing

AI speeds up insurance claims management by using computer vision models to analyze damage photos, cross-referencing policy details, and approving clear-cut claims instantly. This reduces the time it takes to settle simple auto and property claims from weeks to minutes.

Risk Assessment

By moving beyond basic demographic categories, insurers use machine learning to build precise risk profiles. This allows them to price policies dynamically based on actual usage, telematics data from connected cars, and real-time health data from wearables.

Fraud Detection

AI tools flag suspicious insurance claims by identifying hidden connections across multiple files—such as repeated vehicle involvements, suspicious injury timelines, or digital image manipulation in submitted repair photos.

Customer Experience Enhancement

Digital insurance platforms use conversational interfaces to guide users through the process of choosing a policy. This simplifies complex insurance language and matches policy limits to the customer’s actual assets and risks.

Predictive Policy Management

Insurers use predictive models to identify clients who are likely to cancel their policies, allowing teams to proactively reach out with personalized discounts, coverage adjustments, or loyalty programs before renewal dates.

AI in FinTech Startups

Digital Lending

Fintech startups use alternative data scoring engines to build automated lending businesses. By reviewing data like e-commerce revenue and cloud infrastructure spend, these platforms offer non-dilutive working capital loans to digital businesses that traditional banks often overlook.

Embedded Finance

AI APIs let non-financial companies embed banking, payment, and insurance products directly into their own applications. For instance, e-commerce platforms can offer context-aware buy-now-pay-later (BNPL) credit options at checkout by assessing buyer risk instantly.

Payment Innovation

Fintech platforms use machine learning to optimize cross-border payment routes. The system routes payments through different global banking partners in real time based on current processing fees, transaction speeds, and liquidity levels.

Financial Inclusion

By building light, mobile-first risk assessment tools that run on alternative indicators like mobile data usage or micro-merchant transaction histories, fintech startups are bringing secure banking and credit options to unbanked populations globally.

AI-Powered Personal Finance Platforms

Modern personal finance applications act as autonomous money managers. These platforms analyze income schedules and spending habits to automatically calculate, split, and transfer money into optimal savings, investment, and debt-paydown tracks.

Benefits of AI in Finance

Faster Decision-Making

AI compresses core financial timelines. By processing complex data streams instantly, it enables real-time actions like instant mortgage pre-approvals or microsecond trade executions.

Improved Accuracy

Automating manual data entry and reconciliation loops removes human data transcription errors. In risk modeling, multi-variable ML models consistently outperform legacy static spreadsheets.

Enhanced Customer Experience

With AI, consumers get 24/7 support availability, fast transaction processing, and custom financial advice, replacing the slow, rigid workflows of traditional banking.

Reduced Operational Costs

Deploying intelligent automation across back-office tasks allows financial institutions to scale their transaction volumes significantly without a linear increase in administrative headcount.

Better Risk Management

AI scans vast datasets to detect hidden risks early, helping risk managers spot credit downturns, concentration risks, and emerging fraud vectors before they impact the bottom line.

Increased Revenue Opportunities

Advanced data modeling uncovers underserved customer niches, surfaces hyper-targeted cross-selling opportunities, and identifies profitable structural inefficiencies in global capital markets.

Scalable Operations

Digital AI infrastructure processes transaction volume surges without system slowdowns or operational backlogs, giving fintech platforms a highly scalable operating model.

Challenges and Risks of AI in Finance

Data Privacy Concerns

- The Challenge: Financial AI models require massive troves of deeply sensitive personal data, raising significant consumer privacy and data storage safety risks.

- The Solution: Implementing advanced cryptographic techniques like homomorphic encryption and differential privacy, which allow models to train safely on data without exposing personal identifiable information (PII).

Algorithmic Bias

- The Challenge: If historical training data contains human biases against certain demographics, the AI model will learn and reinforce those unfair patterns in loan and credit decisions.

- The Solution: Regular model auditing, utilizing demographic parity metrics, and masking sensitive demographic variables during model training phases.

Regulatory Compliance

- The Challenge: Global financial regulators demand strict oversight, making it difficult for compliance teams to deploy black-box models that cannot be easily audited.

- The Solution: Transitioning to structured model validation frameworks that generate step-by-step audit trails for every automated financial decision.

Cybersecurity Risks

- The Challenge: Bad actors look for ways to exploit AI models through adversarial data injection attacks, which subtly alter inputs to fool fraud or credit risk engines.

- The Solution: Deploying continuous model monitoring, adversarial testing loops, and securing model API access points within zero-trust network environments.

Explainability Challenges

- The Challenge: Deep neural networks can output highly accurate predictions but fail to provide a clear explanation of why a specific decision was made, making it hard to comply with consumer disclosure laws.

- The Solution: Adopting Explainable AI (XAI) frameworks like SHAP (Shapley Additive exPlanations) to break down exactly how much weight each input variable carried in the final output.

Model Drift

- The Challenge: AI models trained under stable market conditions can degrade in accuracy when major macro shifts occur, as the live data stops matching the historical training data.

- The Solution: Setting up automated telemetry alerts that monitor model performance metrics daily and trigger automatic retraining loops when data distribution shifts are detected.

AI Governance and Responsible AI in Finance

Deploying AI safely within regulated financial ecosystems requires a rigorous corporate governance framework. Financial entities cannot treat AI models as autonomous, unaccountable software tools. Responsible AI frameworks rely on four distinct structural pillars:

┌─────────────────────────────────────────────────────────────────────────┐

│ RESPONSIBLE AI GOVERNANCE PILLARS │

├───────────────────┬───────────────────┬───────────────────┬─────────────┤

│ Ethical AI │ Transparency │ Fairness │Accountability│

│ Protects client │ Explains weights │ Audits models for │Clear lines of │

│ welfare & data │ & data lineages │ demographic bias │ human ownership│

└───────────────────┴───────────────────┴───────────────────┴─────────────┘

Regulatory bodies globally have made it clear that final accountability always remains with human leadership teams. If a credit scoring model violates fair lending laws, the institution’s executives are held responsible.

To meet these expectations, forward-thinking organizations deploy independent Model Risk Management (MRM) teams. These teams run validation tests on models before they go live, tracking data provenance, monitoring input drift, and ensuring that every automated financial outcome can be explained to both auditors and clients.

Emerging Trends in AI and Finance

Generative AI for Financial Services

The industry is moving beyond basic chatbots to enterprise-wide generative intelligence platforms. These systems analyze vast document repositories to automatically draft investment memos, generate natural language portfolio updates, and summarize thousand-page regulatory filings for decision-makers.

Autonomous Financial Advisors

The next wave of personal finance features agentic financial paths. These smart systems go beyond simple savings trackers to actively orchestrate your money—navigating taxes, optimizing insurance plans, and shifting capital across asset classes based on your long-term goals with zero manual work required.

AI-Powered Wealth Management

Wealth management is digitizing quickly through hyper-accurate market analysis tools. AI models screen global markets in real time, matching alternative data insights with an investor’s precise tax situation and personal risk preferences to optimize wealth building at scale.

Hyper-Personalized Banking

In the near future, banking portals will adapt entirely to the user. By combining lifestyle data with real-time cash flow analytics, banking apps can predict major financial milestones—like buying a home—and automatically customize the user interface, lending products, and advice to match that exact journey.

Real-Time Risk Intelligence

Risk assessment is shifting from static monthly reviews to continuous, streaming evaluation. Enterprise risk management engines ingest global supply chain data, shifting market rates, and geopolitical news feeds to update institutional risk profiles every minute.

AI and Blockchain Integration

The intersection of AI and decentralized ledger networks provides secure, transparent data infrastructure. Smart contracts use decentralized AI data feeds to automate complex financial agreements safely, while blockchain ledgers provide an unalterable audit trail for tracking AI model training data.

Explainable AI (XAI)

To satisfy strict financial compliance mandates, institutions are prioritizing Explainable AI frameworks. XAI software strips away the mystery of complex black-box neural networks, providing clear maps of exactly which customer or market metrics drove a specific automated decision.

Agentic AI in Financial Operations

The industry is transitioning from isolated AI tasks to fully agentic workflows. These advanced AI agents don’t just surface data—they plan, execute, and verify multi-step back-office operations, such as handling end-to-end invoice reconciliation and cross-border vendor settlements with minimal human intervention.

AI in Finance vs. Traditional Financial Operations

| Operating Area | Traditional Approach | AI-Powered Approach |

| Risk Analysis | Relies on historical, backward-looking spreadsheets and static formulas updated quarterly. | Uses predictive, real-time multi-variable models that ingest streaming market and macro data. |

| Fraud Detection | Depends on rigid, rule-based systems that trigger high numbers of frustrating false positives. | Deploys streaming anomaly detection models that evaluate transaction variables within milliseconds. |

| Customer Service | Operates via limited branch hours and rigid, click-based automated phone trees with long wait times. | Provides 24/7 conversational assistance with contextual memory and multi-step problem resolution. |

| Lending | Evaluates applicants using strict, narrow credit scores, locking out thin-file borrowers. | Evaluates alternative data footprints to expand credit access safely without increasing defaults. |

| Compliance | Requires compliance teams to manually review updated legal filings and corporate policies. | Uses natural language processing to track global regulatory updates and flag policy gaps automatically. |

| Investment Management | Driven by manual research, quarterly rebalancing, and emotional human trading decisions. | Features algorithmic portfolio rebalancing, sentiment analysis, and systematic alternative data screening. |

| Decision Making | Slow, centralized process dependent on batch processing and retrospective review meetings. | Instant, automated decision engines optimized for fast-changing market conditions. |

Real-World Industry Use Cases

Retail Banking

- Challenge: A top-tier consumer bank faced rising customer support costs and dropping user engagement metrics across its mobile platform.

- AI Implementation: The bank deployed a generative AI conversational platform trained on its internal help documentation and connected directly to customer transaction databases via secure APIs.

- Outcome: The AI assistant handled over 65% of incoming support requests on the first interaction, cutting support center costs while driving a 20% increase in mobile app engagement.

Investment Banking

- Challenge: An investment banking deal team was spending thousands of hours manually reviewing contracts and legal filings during mergers and acquisitions due diligence.

- AI Implementation: The firm integrated an enterprise NLP document intelligence platform designed to extract key deal points, liability clauses, and financial covenants from unstructured text.

- Outcome: Due diligence document review timelines were compressed by 75%, allowing deal teams to identify structural risks early and move faster on live transactions.

Insurance

- Challenge: A regional auto insurer was struggling with high claim leakage costs and slow processing timelines due to manual damage vehicle inspections.

- AI Implementation: The insurer launched a mobile-first claims application powered by computer vision models trained on millions of vehicle accident photos.

- Outcome: Customers could submit accident photos via the app and receive automated repair cost estimates and claim approvals within 5 minutes, reducing overall claim cycle times by 70%.

Wealth Management

- Challenge: A wealth management firm found it unprofitable to offer personalized advisory services to mass-affluent investors with smaller capital balances.

- AI Implementation: The firm built a hybrid robo-advisory platform that automates portfolio construction, tax-loss harvesting, and dividend reinvestment using algorithmic models.

- Outcome: The firm lowered its minimum investment threshold, onboarding thousands of new clients and increasing its total Assets Under Management (AUM) without needing to hire more human advisors.

Capital Markets

- Challenge: A systematic trading firm was losing edge because its traditional quantitative models were failing to adapt quickly enough to high-volatility market events.

- AI Implementation: The firm introduced reinforcement learning algorithms that continuously test and adjust trading parameters based on live order book dynamics and execution patterns.

- Outcome: The trading models cut execution slippage costs significantly, maintaining steady performance even during unpredictable, high-volatility market corrections.

FinTech Platforms

- Challenge: A business payment startup was experiencing an increase in sophisticated account takeover attacks that slipped past their traditional password and security rule checks.

- AI Implementation: The platform deployed behavioral biometrics and ML transaction profiling models that analyze subtle user habits, like mouse tracking, typing cadence, and device fingerprints.

- Outcome: Account takeover fraud fell by 85% within the first 90 days of deployment, securing platform workflows without adding annoying login friction for legitimate business users.

Career Opportunities in AI and Finance

The intersection of quantitative finance and artificial intelligence has created an unprecedented demand for cross-disciplinary professionals who can bridge the gap between advanced data science and business-critical financial metrics.

Key Professional Roles

- AI Financial Analyst: Combines traditional valuation skills with automated data processing. They use NLP platforms and predictive models to run large-scale market screens and build advanced corporate forecasting pipelines.

- FinTech Data Scientist: Focuses on designing, training, and testing the core machine learning algorithms that drive business operations, like credit underwriting risk models or real-time fraud mitigation tools.

- Machine Learning Engineer: The software architects who build the infrastructure required to run AI models reliably at scale. They move models from experimental code into high-availability production environments.

- Risk Analytics Specialist: Focuses on system stability and regulatory compliance. They audit automated decision engines for bias, monitor models for input drift, and ensure all AI systems meet governance standards.

- Quantitative Analyst (“Quant”): Designs and deploys mathematical models for pricing complex securities and automating institutional trading strategies across global financial markets.

- AI Product Manager: The strategic bridge between technical engineering teams and business leadership, defining product roadmaps for AI features to ensure they solve real customer problems and hit business goals.

Essential Skill Sets

Building a successful career in this space requires mastering a mix of technical tools and core business concepts:

- Programming & Systems: Proficiency in Python, SQL, and core machine learning libraries (such as PyTorch and Scikit-Learn) alongside cloud data infrastructure platforms like Databricks or AWS.

- Financial Knowledge: A strong understanding of corporate finance, portfolio theory, risk metrics, and the regulatory frameworks that govern banking and securities.

- Data Engineering: The ability to clean, organize, and manage large pipelines of structured and unstructured alternative data.

How to Start Learning AI in Finance

Breaking into this highly competitive field requires a systematic learning strategy that blends foundational mathematics with real-world financial application development.

Step-by-Step Learning Path

┌────────────────────────┐ ┌────────────────────────┐ ┌────────────────────────┐

│ 1. Core Prerequisites │ ───► │ 2. Applied FinTech │ ───► │ 3. Advanced Engineering│

│ • Python & Data Libs │ │ • Quantitative Trading │ │ • GenAI Infrastructure │

│ • Statistical Math │ │ • Credit Risk Modeling │ │ • MLOps & Governance │

│ • Financial Accounting │ │ • NLP Sentiment Engines│ │ • Deployment Pipelines │

└────────────────────────┘ └────────────────────────┘ └────────────────────────┘

1. Master the Prerequisites

Focus first on building a strong foundation in Python programming, mastering data libraries like Pandas and NumPy. Pair this technical training with a solid grasp of statistical mathematics—specifically linear algebra, probability, and regression analysis—while studying the basics of corporate financial accounting and market mechanics.

2. Build Applied Finance Projects

Move beyond textbook theory by working on practical projects with real-world datasets. Try building a credit risk classifier using anonymized peer-to-peer lending data, writing an NLP script that scrapes and scores news headlines for market sentiment, or creating a basic backtesting engine to evaluate an algorithmic trading strategy.

3. Study MLOps and Financial Governance

Learn what it takes to run models in a professional, regulated environment. Study MLOps practices to understand model deployment and tracking, master Explainable AI toolkits like SHAP to make complex models transparent, and learn how to design data pipelines that comply with strict consumer privacy laws.

For comprehensive learning pathways, case studies, and structured technical overviews of modern AI architectures, explore the educational blueprints available on AIUniverse.

Future of AI in Finance

The long-term transformation of financial services points toward a model of autonomous finance. In this future state, routine operations, capital allocation decisions, and systemic risk management loops are managed by interconnected networks of intelligent agents, requiring human intervention only for high-level strategic decisions and ethical oversight.

This shift will not replace human workers; instead, it will elevate their roles. Finance professionals will transition from manual data processors and report builders into strategic AI orchestrators. Human-AI collaboration will become the norm, combining the computing power and pattern recognition of machine learning with the emotional intelligence, creative problem-solving, and moral judgment of human leaders.

As these predictive financial systems mature, they will drastically reduce structural friction, lower transaction costs, and make high-quality, personalized wealth-building strategies accessible to millions of people globally.

FAQ Section

What is AI in finance?

AI in finance refers to the strategic integration of machine learning algorithms, natural language processing, predictive analytics, and generative models into financial operations to automate workflows, identify risks, and optimize asset management.

How is AI used in banking?

Banks deploy AI for real-time transaction monitoring to stop fraud, automated credit underwriting, conversational customer support assistants, and personalized marketing recommendations within mobile banking applications.

Can AI predict stock market movements?

AI cannot predict future market movements with absolute certainty. However, it can identify complex historical patterns, analyze alternative data streams, and evaluate market sentiment to help investment teams make better risk-adjusted decisions.

Is AI replacing financial analysts?

No, AI is not replacing financial analysts; it is changing their day-to-day responsibilities. By automating repetitive data compilation tasks, AI allows analysts to focus on higher-value activities like strategic planning and nuanced investment judgment.

What are the risks of AI in finance?

The primary risks include algorithmic bias in credit decisions, model degradation during unexpected market shifts, data privacy leaks, cybersecurity vulnerabilities, and compliance challenges stemming from opaque “black-box” models.

How does AI detect fraud?

AI detects fraud by analyzing millions of transaction variables simultaneously in real time—evaluating metrics like spending velocity, geographic location, and historical behavioral footprints to block anomalies before processing finishes.

What skills are needed for AI finance careers?

Professionals need a strong mix of Python programming, statistical data analysis, machine learning model architecture knowledge, corporate finance fundamentals, and an understanding of financial regulatory compliance frameworks.

What is generative AI in finance?

Generative AI in finance uses advanced deep learning models trained on text and financial data to summarize long regulatory documents, synthesize portfolio performance narratives, generate synthetic data for stress testing, and draft investment memos.

Is AI safe for financial decision-making?

AI is safe for financial decision-making only when deployed within a strict corporate governance framework that includes continuous model auditing, clear explainability guardrails, and consistent human-in-the-loop oversight.

How are banks using machine learning?

Banks use machine learning to process unstructured alternative data for credit scoring, automate anti-money laundering transaction tracking, forecast internal liquidity requirements, and optimize back-office administrative workflows.

What is Explainable AI (XAI) in finance?

Explainable AI is a set of tools and frameworks that allows data scientists and compliance teams to explain exactly why a complex machine learning model arrived at a specific credit, risk, or investment output.

What is alternative data in AI finance?

Alternative data refers to non-traditional financial information used by AI models to evaluate risks or investments. This includes data streams like satellite imagery of retail parking lots, shipping manifests, and utility payment histories.

How does AI improve credit scoring?

AI improves credit scoring by analyzing non-traditional financial behaviors, allowing institutions to accurately assess the creditworthiness of thin-file or unbanked individuals who lack standard credit bureau histories.

What is RegTech and how does AI empower it?

RegTech stands for Regulatory Technology. AI empowers RegTech by using natural language processing to scan global legal updates continuously, automatically updating internal institutional compliance policies and tracking systemic risks.

What is agentic AI in financial operations?

Agentic AI refers to independent AI systems designed to plan, execute, and verify multi-step workflows—such as automated invoice reconciliation or cross-border payment routing—with minimal manual human intervention.

Final Summary

The structural integration of artificial intelligence is fundamentally changing how global financial services operate. Core technologies like machine learning, natural language processing, and generative AI have moved past the pilot phase to drive real-world transformation across the banking, insurance, and investment sectors. By automating complex workflows, mitigating fraud risks, and unlocking hidden revenue opportunities, AI platforms provide a clear and durable competitive advantage.

While issues like data privacy, model drift, and algorithmic bias require careful management, the industry is moving steadily toward an era of autonomous, highly efficient finance. Organizations that prioritize data engineering, implement robust governance frameworks, and upskill their workforces will lead this digital evolution, while those clinging to legacy systems risk falling behind.